If you’re asking what is reference-based pricing, the short answer is that it is a healthcare reimbursement strategy commonly used with self-funded health plans. Instead of relying solely on negotiated provider contracts, reference-based pricing reimburses healthcare providers using a predetermined benchmark—often a percentage of Medicare reference pricing. This approach can provide employers with greater healthcare transparency and more predictable reimbursement methodologies while supporting broader healthcare cost containment efforts.

As healthcare costs continue to rise, many employers, HR professionals, CFOs, and benefits brokers are exploring alternative approaches to managing an employer-sponsored health plan. While reference-based pricing is not the right fit for every organization, it can be one component of a customized benefits strategy when paired with experienced administration, clear employee communication, and thoughtful plan design.

In this guide, we’ll explain how reference-based pricing works, how providers are reimbursed, how it compares with traditional PPO networks, and the important role a third-party administrator plays in administering these plans.

What Is Reference-Based Pricing?

Reference-based pricing is a reimbursement methodology that determines how much a health plan pays for covered medical services based on a defined benchmark rather than relying exclusively on negotiated provider network contracts.

In many reference based pricing health insurance arrangements, the benchmark is tied to Medicare reference pricing, such as a specified percentage above current Medicare reimbursement rates. However, reimbursement methodologies vary by plan, employer, and administrator, and not every plan uses the same formula.

For employers, the primary goal is greater transparency around healthcare reimbursement. Instead of paying prices established through negotiated network contracts, the plan uses a consistent reimbursement methodology that employers can better understand and monitor over time.

Reference-based pricing is most commonly associated with self-funded health plans, where employers assume responsibility for eligible claims while maintaining greater flexibility in plan design. Many organizations work with an experienced third-party administrator or TPA to administer these plans, coordinate claims, support employees, and manage provider communication.

Rather than viewing reference-based pricing as a replacement for every traditional reimbursement model, employers often evaluate it as one tool within a broader healthcare strategy focused on transparency, flexibility, and long-term plan management.

Reference-based pricing establishes provider reimbursement using a defined benchmark, giving employers greater visibility into how medical claims are paid.

How Does Reference-Based Pricing Work?

Understanding the process can make reference-based pricing much easier to evaluate. While plan designs differ, the overall workflow generally follows the same sequence.

Step 1: The Employee Receives Care

An employee covered by the employer health plan visits a physician, hospital, or other healthcare provider for covered medical services.

Step 2: The Provider Submits the Claim

After treatment, the provider submits a medical claim to the plan for reimbursement, just as they would with many other health plans.

Step 3: Claims Administration Reviews the Claim

The plan’s claims administration team reviews the claim to verify eligibility, apply plan provisions, and confirm that the services qualify for reimbursement.

This review also ensures accurate medical claims pricing and compliance with the employer’s benefit plan.

Step 4: The Reimbursement Benchmark Is Applied

Instead of relying solely on a negotiated PPO contract rate, the plan calculates provider reimbursement using its established reference-based pricing methodology.

Many plans use a multiple of Medicare reimbursement as the benchmark, although reimbursement formulas differ depending on the employer’s plan design.

Step 5: Payment Is Issued

Once the review is complete, payment is issued according to the plan’s reimbursement methodology.

Throughout this process, the TPA may coordinate communication between the employer, healthcare providers, and plan members while ensuring claims are processed consistently.

Because reimbursement methodologies differ, employee education and provider communication remain important parts of successful implementation.

Reference-based pricing follows a familiar claims process, but the reimbursement calculation is based on a predetermined benchmark rather than only negotiated provider contracts.

Why Employers Consider Reference-Based Pricing

Healthcare benefits represent one of the largest operating expenses for many organizations. As medical inflation, hospital pricing, and prescription drug costs continue to increase, employers are looking for strategies that can help them better understand and manage long-term spending.

Reference-based pricing is often evaluated because it may offer:

- Greater healthcare transparency

- More consistent healthcare reimbursement methodologies

- Increased visibility into medical claims pricing

- Additional flexibility within self-funded health plans

- Support for broader healthcare cost containment initiatives

Rather than focusing exclusively on short-term plan cost savings, many employers view reference-based pricing as a way to improve long-term decision-making through better reporting and reimbursement visibility.

Benefits brokers frequently help employers evaluate whether reference-based pricing aligns with their workforce, financial objectives, and employee benefits strategy. Since every organization has different goals and risk considerations, a careful evaluation is essential before making changes to an employer-sponsored health plan.

It’s also important to recognize that reference-based pricing is only one component of a comprehensive benefits strategy. Other elements—such as claims administration, care management, pharmacy management, and employee communication—continue to play significant roles in overall plan performance.

Employers often explore reference-based pricing to improve transparency and gain greater insight into healthcare spending, not because it is a universal solution.

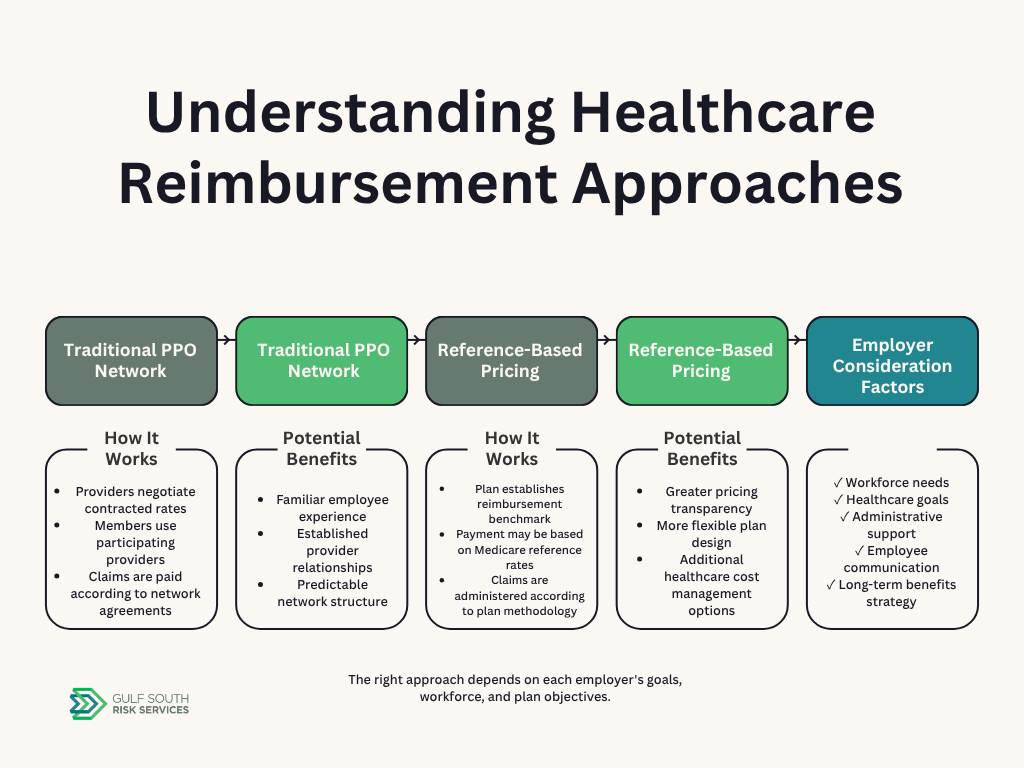

Reference-Based Pricing vs. PPO Networks

One of the most common questions employers ask is whether reference-based pricing replaces a traditional PPO network. The answer depends on the specific health plan.

A PPO alternative does not necessarily eliminate provider networks altogether. Some employers use reference-based pricing alongside selected network solutions, while others incorporate different reimbursement strategies depending on the services being provided.

The biggest distinction is how providers are reimbursed.

With a traditional PPO network, providers generally agree to contracted reimbursement rates through negotiated agreements. Under reference-based pricing, reimbursement is based on the methodology established by the employer’s health plan rather than negotiated network discounts.

Comparison: Reference-Based Pricing vs. PPO Networks

| Feature | Reference-Based Pricing | Traditional PPO Network |

| Reimbursement Method | Defined benchmark | Negotiated provider contracts |

| Pricing Visibility | Often greater transparency | Contract rates determined through network agreements |

| Provider Contracts | May vary by plan | Established PPO agreements |

| Employer Flexibility | Often greater customization | Typically tied to network structure |

| Administration | Coordinated by the TPA | Coordinated by carrier or administrator |

| Member Experience | Depends on communication and plan design | Familiar network-based experience |

Neither approach is inherently better for every employer. The most appropriate reimbursement model depends on workforce needs, organizational goals, provider access, administrative resources, and the overall design of the health plan.

Reference-based pricing and PPO networks represent different reimbursement strategies, and many employers evaluate them as part of a broader benefits discussion rather than viewing them as direct replacements.

What Role Does a Third-Party Administrator Play?

A successful reference-based pricing strategy relies on more than a reimbursement formula. Experienced administration, communication, and ongoing support are essential.

An experienced third-party administrator helps coordinate many of the operational responsibilities associated with administering these plans, including:

- Claims administration

- Provider communication

- Member support

- Eligibility verification

- Reporting and analytics

- Care coordination

- Administrative compliance

- Health plan administration

Because independent TPAs are focused on administration rather than assuming insurance risk, they often help employers integrate multiple vendors, reporting platforms, and healthcare resources into one coordinated program.

Gulf South Risk Services serves as an experienced independent administrator for employers, brokers, municipalities, school districts, healthcare organizations, and other clients evaluating customized health plan solutions. Through flexible plan administration, transparent reporting, and responsive member service, Gulf South helps organizations evaluate reimbursement strategies that align with their employee benefits goals.

Just as importantly, TPAs help facilitate communication among employers, providers, and employees throughout the claims process. Clear communication can improve the member experience and help address questions about reimbursement methodologies before they become larger administrative issues.

A knowledgeable TPA provides the administrative expertise, reporting, communication, and coordination that help employers effectively manage reference-based pricing within a broader health plan strategy.

Advantages of Reference-Based Pricing

When thoughtfully designed and properly administered, reference-based pricing can provide employers with several potential advantages. However, the impact of any reimbursement strategy depends on the employer’s goals, workforce, plan design, and administrative approach.

One potential advantage is increased healthcare transparency. Traditional healthcare pricing can vary significantly between providers, and employers may have limited visibility into how reimbursement rates are established. A defined reimbursement methodology can provide a clearer framework for understanding healthcare spending.

Reference-based pricing may also provide greater flexibility for self-funded health plans. Because self-funded employers are responsible for funding claims, they often have more opportunities to customize plan structures, evaluate different vendor solutions, and align benefits strategies with organizational objectives.

Additional potential benefits include:

- Improved visibility into healthcare spending

- More predictable reimbursement methodologies

- Greater employer involvement in plan design

- Additional options for healthcare cost containment

- Opportunities to evaluate provider pricing trends

- Increased access to claims data and reporting

For benefits brokers, reference-based pricing can become another option to discuss when helping employers evaluate healthcare strategies. A broker can help assess whether this approach aligns with employee needs, financial goals, and long-term benefits objectives.

Reference-based pricing may also work alongside other healthcare management strategies, including utilization management, case management, pharmacy oversight, and employee education.

Reference-based pricing can provide employers with additional transparency and flexibility, but its effectiveness depends on thoughtful implementation and ongoing administration.

Important Considerations Before Implementing Reference-Based Pricing

While reference-based pricing can provide advantages, employers should carefully evaluate potential challenges before implementing this type of reimbursement strategy.

One important consideration is employee education. Employees are accustomed to traditional insurance models where provider networks and negotiated rates are familiar. A reference-based pricing model may require additional communication to help employees understand how reimbursement works and what steps to take when receiving care.

Provider communication is another important factor. Not every provider may immediately understand or accept a reference-based pricing arrangement, and reimbursement discussions may occur between providers, administrators, and members depending on the circumstances.

Employers should also consider:

Administration Requirements

Reference-based pricing requires experienced claims administration, clear processes, and effective communication. A knowledgeable administrator can help coordinate claims review, provider questions, and member support.

Member Support

Employees may have questions about provider reimbursement, medical bills, and healthcare costs. Strong customer service and education resources are important parts of the employee experience.

Plan Design

Reference-based pricing should be evaluated within the context of the entire employer health plan. Employers should consider their workforce demographics, healthcare utilization patterns, and benefit objectives.

Provider Relationships

The provider experience can vary depending on geographic location, healthcare market conditions, and reimbursement practices.

Additional Plan Components

Reference-based pricing may be combined with other strategies, such as:

- PPO networks

- Pharmacy Benefit Manager (PBM) partnerships

- Stop-loss insurance

- Utilization management

- Case management

- Care coordination

A balanced evaluation helps employers determine whether reference-based pricing fits their specific circumstances.

Reference-based pricing requires education, communication, and experienced administration to support both employers and employees.

Is Reference-Based Pricing Right for Every Employer?

Reference-based pricing is not automatically the right choice for every organization. Employers should evaluate the approach based on their unique workforce, financial goals, and benefits strategy.

Organizations that may explore reference-based pricing often include:

- Self-funded employers seeking greater pricing transparency

- Employer groups reviewing healthcare cost management options

- Organizations evaluating alternatives to traditional PPO structures

- Public entities and educational organizations exploring customized benefits solutions

Important factors to consider include:

Company Goals

Employers should determine whether their primary objectives include greater transparency, plan flexibility, improved reporting, or broader cost management strategies.

Workforce Characteristics

Employee location, healthcare needs, demographics, and provider preferences can influence whether a reimbursement strategy is appropriate.

Current Healthcare Spending

Understanding existing claims trends, high-cost claims, utilization patterns, and healthcare expenses provides important context.

Administrative Support

A strong administrative partner can help employers evaluate options, implement plan changes, and support employees throughout the process.

Benefits brokers often play a key role by helping organizations compare alternatives and determine which approach best supports their long-term objectives.

Reference-based pricing should be evaluated as part of a broader benefits strategy—not adopted simply because it is used by other employers.

Choosing the Right Administrative Partner

The success of any self-funded health plan strategy depends heavily on effective administration. Employers considering reference-based pricing should evaluate potential partners based on experience, service capabilities, and operational support.

Important evaluation criteria include:

Claims Administration Experience

Look for an administrator with experience managing complex medical claims, reimbursement methodologies, and employer benefit programs.

Communication Capabilities

Strong communication with employers, employees, brokers, and providers is essential. Clear explanations can help reduce confusion and improve the member experience.

Reporting and Analytics

Employers should evaluate whether the administrator provides meaningful reporting related to:

- Claims activity

- Healthcare utilization

- Provider reimbursement

- Plan performance

- Cost trends

Technology Integration

A capable administrator should be able to coordinate with healthcare vendors, including:

- Pharmacy Benefit Managers

- PPO networks

- Stop-loss insurance carriers

- Care management providers

- Reporting platforms

- Flexibility

Because every employer has different goals, administrative flexibility is important. Employers should look for partners that support customized plan design rather than forcing every organization into the same model.

Gulf South Risk Services provides independent administration focused on flexibility, service, and long-term partnerships. By supporting health plan administration, claims management, vendor coordination, and member services, Gulf South helps employers and brokers evaluate customized solutions that fit their objectives.

The right administrative partner provides more than processing support—it provides guidance, communication, and operational expertise.

Final Thoughts

Understanding what is reference-based pricing requires looking beyond the reimbursement formula. Reference-based pricing is one approach employers may consider when evaluating self-funded health plans, healthcare transparency, and long-term healthcare cost containment strategies.

When combined with experienced administration, employee education, strong communication, and thoughtful plan design, reference-based pricing can provide employers with greater visibility into healthcare reimbursement and spending.

However, it is not a universal solution. Employers should carefully evaluate their workforce, goals, administrative needs, and risk considerations before making changes to their employer-sponsored health plan.

Gulf South Risk Services helps employers and brokers evaluate customized health plan administration strategies, including claims administration, cost containment solutions, and flexible benefit program support.

Contact Gulf South Risk Services to learn more about health plan administration and how customized solutions may support your organization’s employee benefits goals.

Frequently Asked Questions

What is reference-based pricing?

Reference-based pricing is a healthcare reimbursement strategy that uses a predetermined benchmark to determine how much a health plan pays for covered medical services. Many plans use a percentage of Medicare reimbursement rates as a reference point, although methodologies vary by plan design.

How is provider reimbursement calculated?

Provider reimbursement under reference-based pricing is calculated using the methodology established by the health plan. Some plans use Medicare reimbursement as a benchmark, while others may use different formulas. The specific approach depends on the employer’s plan design and administrative structure.

Is reference-based pricing only for self-funded plans?

Reference-based pricing is most commonly associated with self-funded health plans because employers have greater flexibility in designing reimbursement strategies. However, the suitability of any approach depends on the organization’s goals, resources, and benefit structure.

Can employees still choose their providers?

Employee provider access depends on the specific plan design. Some reference-based pricing arrangements allow broad provider choice, while others may incorporate networks or additional provider access strategies. Employees should review their plan information before receiving care.

Does reference-based pricing replace PPO networks?

Not necessarily. Some employers use reference-based pricing as an alternative to traditional PPO reimbursement, while others combine different approaches. A PPO network may still be part of a broader benefits strategy depending on the plan design.

What role does a TPA play in reference-based pricing?

A TPA supports the administration of reference-based pricing by managing claims administration, member communication, reporting, provider coordination, eligibility management, and other operational responsibilities.

Is reference-based pricing appropriate for every employer?

No. Employers should evaluate factors such as workforce demographics, healthcare goals, claims experience, administrative capabilities, and employee communication needs before determining whether reference-based pricing fits their organization.