Employee benefits administration can be complex, especially when employers are evaluating how health plans are structured and managed. Organizations often encounter both Third Party Administrator (TPA) organizations and insurance carriers, but the roles they play are not always clearly understood. This confusion can make it difficult for HR leaders, CFOs, and benefits managers to determine how employee health plans actually operate behind the scenes.

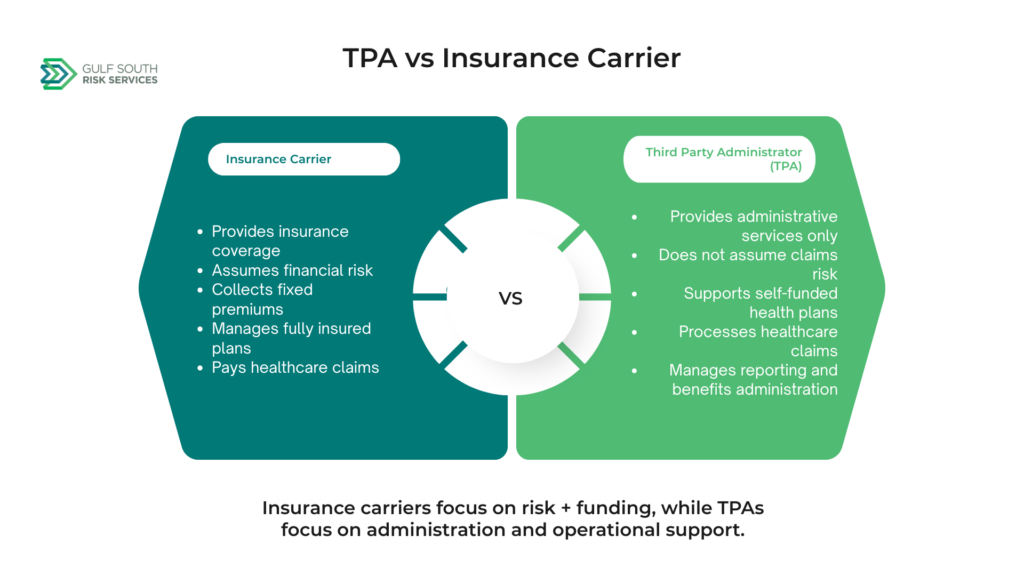

In simple terms, the difference in TPA vs Insurance Carrier comes down to responsibility and function. Insurance carriers typically assume financial risk under fully insured arrangements, while TPAs focus on administering health plans, particularly within Self Funded Health Plans, where the employer retains responsibility for claims costs.

This article explains how each entity works, how claims are handled, and how they fit into modern Health Plan Administration models. It also helps decision-makers understand how TPA Services support organizations managing employee benefits.

Have questions about employee benefits administration? Contact Gulf South Risk Services to learn more about TPA services and self-funded health plans.

What Is a Third Party Administrator (TPA)?

A Third Party Administrator (TPA) is an organization that manages administrative functions for employee benefit plans on behalf of an employer. A TPA does not typically provide insurance coverage or assume claims risk. Instead, it focuses on the operational side of Employee Benefits Administration.

TPAs commonly support Self Funded Health Insurance arrangements where the employer pays healthcare claims directly. Their responsibilities often include:

- Healthcare claims processing

- Benefits administration

- Customer service for members

- Eligibility and enrollment management

- Reporting and analytics

- Coordination of Claims Administration Services

In this model, the TPA acts as the operational backbone of the plan, ensuring that claims are processed correctly and members receive support while the employer retains financial responsibility for claims.

What Is an Insurance Carrier?

An Insurance Carrier is a licensed insurance company that provides coverage under a fully insured health plan. In this arrangement, the employer pays fixed premiums, and the carrier assumes responsibility for covered healthcare claims.

Insurance carriers typically:

- Collect premiums from employers

- Assume financial risk for claims

- Operate fully insured health plans

- Maintain provider networks

- Handle claims payments directly

In traditional Employer Sponsored Health Plans, the carrier is responsible for both funding and managing claims within the policy structure. This model differs significantly from self-funded arrangements where employers retain risk.

The Biggest Difference: Who Assumes Financial Risk?

The core distinction in TPA vs Insurance Carrier is risk assumption.

Fully Insured Plans (Insurance Carrier Model)

- Insurance carrier assumes all claims risk

- Employer pays fixed monthly premiums

- Carrier manages and funds claims

Self-Funded Plans (TPA Model)

- Employer assumes financial responsibility for claims

- TPA handles administration only

- Stop-loss insurance may help protect against high-cost claims

Simple Breakdown:

Insurance Carrier = Risk + Administration

TPA = Administration only (in most self-funded arrangements)

This separation of roles is a key reason many organizations evaluate Self Funded Health Plan structures when reviewing long-term benefits strategy.

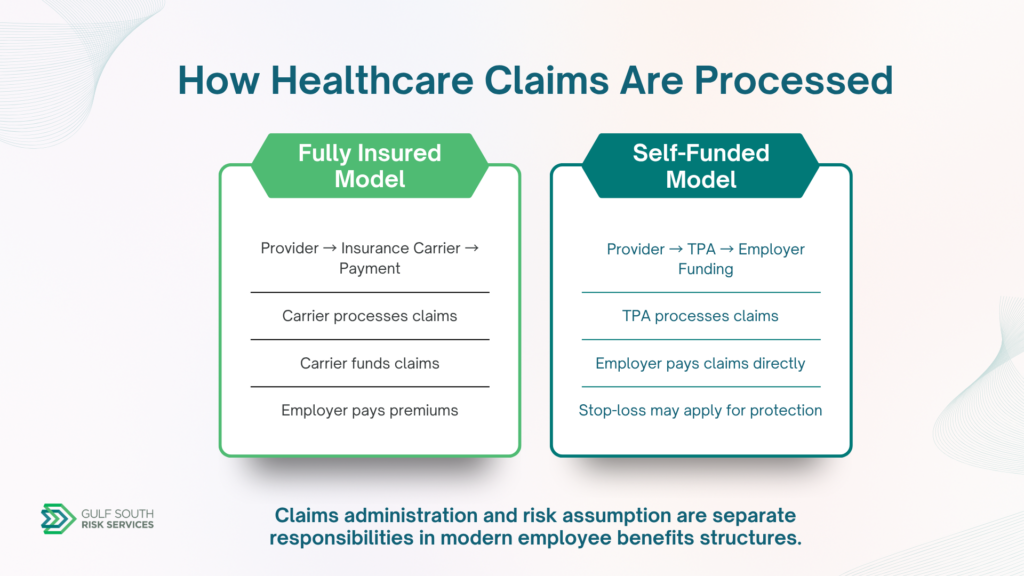

How Claims Administration Works

Understanding Healthcare Claims Processing helps clarify the operational difference between TPAs and insurance carriers.

Under a Fully Insured Plan:

- Insurance carrier receives claims from providers

- Carrier processes and adjudicates claims

- Carrier pays claims using premium dollars

- Under a Self-Funded Plan:

- Healthcare providers submit claims

- TPA processes and reviews claims

- Employer funds approved claims directly

- Stop-loss insurance may apply for high-cost cases

In this structure, Benefits Administration and claims oversight are handled by the TPA, while financial responsibility remains with the employer.

What Services Does a TPA Typically Provide?

TPAs offer a wide range of administrative and operational services that support self-funded arrangements:

- Claims administration and adjudication

- Member support and customer service

- Benefits administration and eligibility management

- Reporting and data analytics

- Cost containment program support

- Provider network coordination

- Compliance and regulatory support

These services allow employers to maintain control over plan design while outsourcing complex administrative tasks.

Which Organizations Commonly Work With TPAs?

Organizations that evaluate TPA Services often include:

- Municipalities

- School districts

- Mid-sized employers

- Healthcare organizations

- Self-funded employers

These organizations frequently explore self-funding because it can offer more flexibility in plan design and access to detailed claims data. However, the decision is typically based on financial strategy, workforce needs, and risk tolerance rather than organization size alone.

How TPAs Support Self Funded Health Plans

TPAs play a central role in supporting Self Funded Health Insurance programs by providing operational expertise and administrative infrastructure.

Key support areas include:

- Claims management and processing

- Employee Benefits Administration

- Reporting and data analytics

- Compliance monitoring

- Vendor and provider coordination

- Cost containment support

Many organizations rely on TPAs as a core component of Health Plan Administration to ensure efficiency and consistency across the benefits ecosystem.

Advantages of Greater Claims Visibility

One of the most notable differences in self-funded arrangements is access to data.

Employers working with a TPA often gain visibility into:

- Claims trends and patterns

- Healthcare utilization data

- Cost drivers within the plan

- Reporting dashboards and analytics

This level of transparency can support more informed decision-making in Benefits Management and long-term healthcare strategy planning. Rather than focusing on savings alone, visibility allows organizations to better understand how benefits are being used.

Common Misconceptions About TPAs

TPAs Are Insurance Companies

False. TPAs do not typically provide insurance coverage or assume claims risk.

TPAs Assume Claims Risk

Not typically. In most self-funded models, the employer retains financial responsibility.

TPAs Only Serve Large Employers

Incorrect. TPAs support organizations of many sizes, including municipalities and mid-sized employers.

TPAs Replace Insurance Entirely

Not accurate. Many self-funded plans still rely on stop-loss insurance and other risk management tools.

Understanding these distinctions helps clarify how Insurance Carrier and TPA roles differ within modern benefit structures.

Questions Employers Should Ask When Evaluating Plan Options

- Who assumes claims risk?

- How are claims administered?

- What reporting is available?

- What support services are included?

- What are our long-term benefits goals?

Understanding how employee benefits are administered can help organizations make informed decisions about future plan structures.

Which Model Is Right for Your Organization?

There is no universal answer when comparing TPA vs Insurance Carrier models. The right structure depends on several factors:

- Organizational goals and benefit strategy

- Workforce size and demographics

- Administrative preferences

- Risk tolerance and financial capacity

- Desire for claims transparency and reporting

Some organizations prefer the predictability of fully insured coverage, while others value the flexibility and visibility associated with self-funded arrangements supported by a TPA.

Conclusion

The difference between a Third Party Administrator and an Insurance Carrier is primarily defined by function and financial responsibility. Insurance carriers typically assume risk and provide fully insured coverage, while TPAs focus on administering plans, particularly within Self Funded Health Plans, where employers retain claims responsibility.

Understanding how these roles differ helps employers evaluate Employee Benefits Administration strategies more effectively and choose structures that align with their organizational goals.

Contact Gulf South Risk Services to learn more about TPA services, claims administration, and self-funded health plan support.