If you’ve ever wondered what does a third-party administrator do, the short answer is this: a third-party administrator (TPA) manages the day-to-day administration of employer health plans and workers’ compensation programs. Rather than simply processing claims, today’s TPAs coordinate benefits administration, medical claims processing, customer service, reporting, vendor relationships, and cost containment while helping employers maintain flexibility and oversight of their benefit programs.

As more organizations evaluate self-funded health plans and customized employee benefits strategies, understanding the role of a third-party administrator has become increasingly important. Employers, HR professionals, CFOs, and benefits brokers often encounter TPAs when exploring alternatives to traditional insurance arrangements, but many are surprised by the breadth of services an independent administrator can provide.

This guide explains how a modern TPA works, what services it provides, how it supports employers and brokers, and why independent TPAs have become valuable operational partners for organizations seeking greater flexibility in health plan administration and workers’ compensation programs.

What Is a Third-Party Administrator?

A third-party administrator (TPA) is an independent organization that manages the administrative operations of employer-sponsored health plans and other benefit programs on behalf of employers, brokers, public entities, and organizations.

Unlike an insurance company, a TPA generally does not insure risk or issue insurance policies. Instead, it provides plan administration services that help employers efficiently operate their benefit programs.

Organizations that commonly hire a TPA include:

- Self-funded employers

- Municipalities

- School districts

- Healthcare organizations

- Business owners

- Employee benefits brokers

For employers with a self-funded health plan, the employer typically funds healthcare claims while the TPA manages the administrative responsibilities associated with the plan.

Those responsibilities often include claims administration, eligibility management, customer service, reporting, compliance support, and coordination with healthcare vendors.

As an independent TPA, Gulf South Risk Services provides administrative expertise while allowing employers and brokers to maintain flexibility in selecting vendors, provider networks, and plan partners that align with their objectives.

A TPA administers benefit programs—it is not the insurance company responsible for assuming financial risk.

What Services Does a Third-Party Administrator Provide?

Many people believe a TPA’s primary responsibility is processing claims. In reality, modern TPAs manage a broad ecosystem of administrative and operational services that support employers, employees, brokers, and healthcare vendors.

Common services include:

Health Plan Administration

Effective health plan administration involves coordinating the day-to-day operations of employer-sponsored health plans, including eligibility management, enrollment support, plan maintenance, and ongoing administrative oversight.

Claims Administration

One of the most visible TPA responsibilities is claims administration. This includes reviewing submitted healthcare claims, applying plan rules, coordinating payment processes, and ensuring accurate medical claims processing.

Claims administration also involves documentation, communication, and ongoing monitoring throughout the life of a claim.

Employee Benefits Administration

Comprehensive employee benefits administration includes:

- Eligibility management

- Enrollment support

- Member communications

- Benefit questions

- ID card administration

- Ongoing customer support

Employees often interact with the TPA whenever they need assistance understanding or using their health benefits.

Customer Service

Customer service remains one of the most valuable functions provided by an independent TPA.

Dedicated service teams help members:

- Understand benefits

- Resolve claim questions

- Navigate healthcare services

- Coordinate with providers

- Address administrative concerns

Responsive communication helps improve the member experience while reducing administrative burdens for employers.

Reporting and Analytics

TPAs provide employers with reporting that may include:

- Claims trends

- Healthcare utilization

- High-cost claim analysis

- Population health insights

- Plan performance metrics

This visibility allows employers to better understand how their benefit plans are performing over time.

Utilization Management and Case Management

Many TPAs coordinate utilization management programs that review healthcare utilization patterns and support appropriate care.

They may also oversee case management services for employees with complex medical needs, helping coordinate care, improve communication, and support better health outcomes.

Vendor Coordination

A modern TPA often serves as the central point of coordination among multiple healthcare partners, ensuring consistent administration across the benefit ecosystem.

A TPA manages far more than claims—it supports nearly every operational aspect of an employer health plan.

How Does a TPA Work With Self-Funded Health Plans?

A self-funded health plan operates differently from a traditional fully insured plan.

Instead of paying fixed premiums to an insurance carrier that assumes claims risk, the employer funds eligible healthcare claims directly. The TPA administers the plan on the employer’s behalf.

This arrangement allows employers to maintain greater flexibility in areas such as:

- Plan design

- Vendor selection

- Reporting

- Benefits administration

- Provider network options

Rather than operating within a predefined carrier model, employers can often customize programs around their workforce and organizational goals.

Benefits brokers also play an important role by helping employers evaluate plan options and coordinate with TPAs to develop benefit strategies that meet client needs.

An independent administrator like Gulf South Risk Services supports these programs through administrative expertise while allowing employers to retain greater visibility into claims activity and overall plan performance.

In a self-funded model, employers fund claims while the TPA manages the day-to-day administration.

How TPAs Support Employee Benefits Brokers

Benefits brokers are trusted advisors for employers evaluating health plans, workers’ compensation programs, and long-term benefits strategies. An experienced TPA works alongside—not in place of—the broker.

Strong broker partnerships are built on collaboration rather than competition.

Independent TPAs help brokers by providing:

- Administrative expertise

- Flexible plan administration

- Customized reporting

- Responsive customer service

- Vendor coordination

- Claims administration support

Because independent TPAs are not tied to a single insurance carrier, brokers often have greater flexibility when recommending provider networks, vendors, and benefit solutions that align with each client’s objectives.

This flexibility allows brokers to tailor solutions without being limited to one proprietary ecosystem.

Gulf South Risk Services has long emphasized a broker-first philosophy by supporting broker relationships, providing personalized service, and acting as an extension of both the broker’s and employer’s teams.

Independent TPAs strengthen broker relationships by providing administrative expertise while allowing brokers to maintain ownership of the client relationship.

How TPAs Help Control Healthcare Costs

A TPA cannot eliminate healthcare costs or guarantee savings. However, effective administration can help employers better understand healthcare spending and identify opportunities to improve plan performance.

Common areas of support include:

Claims Reporting

Detailed reporting provides employers with visibility into healthcare utilization, claims trends, and plan performance.

Utilization Management

Reviewing treatment patterns and healthcare utilization may help ensure services are appropriate while supporting quality care.

Case Management

Coordinating complex medical cases can improve communication among providers, employees, and employers throughout the treatment process.

Provider Networks and PPOs

Many TPAs coordinate with PPO networks that provide employers and members access to contracted healthcare providers.

Pharmacy Management

TPAs frequently coordinate with a pharmacy benefit manager (PBM) to administer pharmacy benefits, review prescription utilization, and support pharmacy program management.

Reference-Based Pricing

Some employers may explore reference-based pricing as one component of a broader healthcare strategy, depending on their plan structure and goals.

Rather than focusing solely on expense reduction, these programs support informed decision-making, improved transparency, and long-term healthcare management.

Cost containment is most effective when supported by data, oversight, and coordinated plan administration.

Technology and Vendor Integration

One of the defining characteristics of a modern independent TPA is the ability to integrate multiple vendors and technologies into a single administrative framework.

Rather than requiring employers to use one proprietary system, independent TPAs often coordinate with:

- Pharmacy benefit managers (PBMs)

- PPO networks

- Stop-loss insurance providers

- Care management vendors

- Reporting platforms

- Claims technology systems

Gulf South Risk Services uses a flexible “hub-and-spoke” administrative approach that centralizes administration while allowing employers and brokers to select best-in-class partners based on their individual needs.

This flexibility helps organizations adapt as their programs evolve without requiring a complete administrative overhaul.

Technology integration allows employers to customize benefit programs while maintaining consistent administration through a single operational partner.

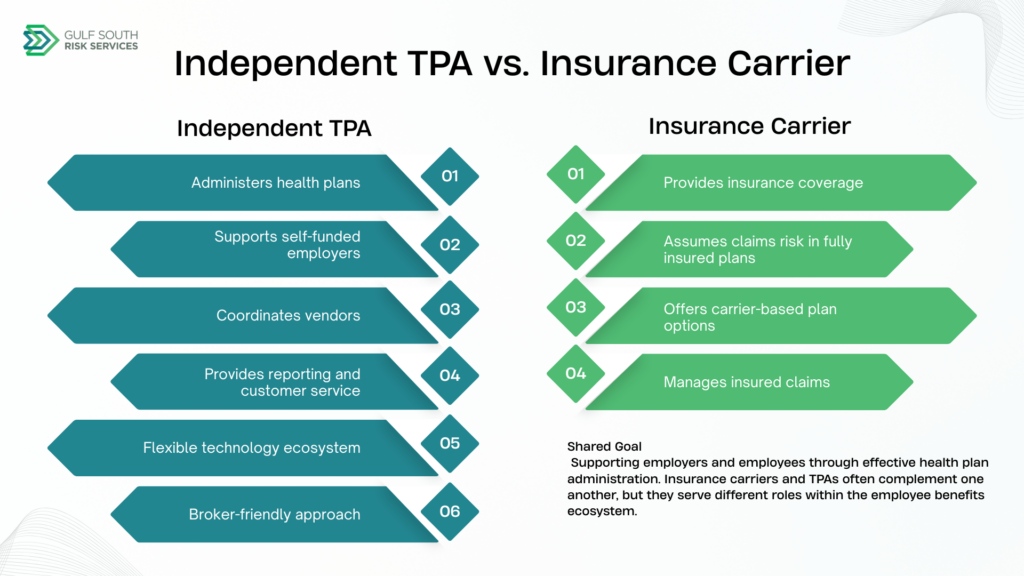

Independent TPA vs. Insurance Carrier

One of the most common misconceptions is that a TPA and an insurance carrier perform the same function. While they often work within the same employee benefits ecosystem, their responsibilities are fundamentally different.

An insurance carrier generally assumes financial risk under a fully insured plan. A third-party administrator, on the other hand, focuses on administering the plan. In a self-funded health plan, the employer typically retains responsibility for eligible claims while the TPA manages day-to-day operations.

Independent TPAs also tend to offer greater flexibility because they are not tied to a single insurance company’s products, provider networks, or technology platforms. This allows employers and brokers to build programs around their specific goals rather than fitting into a predefined carrier model.

| Feature | Independent TPA | Insurance Carrier |

| Primary Role | Administration | Insurance coverage and risk assumption |

| Claims Responsibility | Administers claims | Pays claims in fully insured plans |

| Flexibility | High vendor flexibility | Often tied to proprietary solutions |

| Plan Customization | Greater customization opportunities | Typically standardized options |

| Vendor Selection | Employer and broker choose vendors | Often carrier-selected |

| Customer Service | Dedicated administrative support | Carrier service model |

| Best Fit | Self-funded and customized plans | Fully insured plans |

It’s also important to remember that TPAs do not replace insurance entirely. Many self-funded employers work with stop-loss insurance providers to help protect against catastrophic claims while continuing to use a TPA for administration.

Insurance carriers primarily insure risk, while independent TPAs provide administrative expertise and operational support.

When Should an Employer Consider Working With a TPA?

There is no single point at which every organization should work with a TPA. However, employers often begin exploring administration options when they experience changes in their workforce, benefits strategy, or healthcare costs.

Organizations may consider partnering with a TPA when they:

- Are evaluating a self-funded health plan

- Want more flexibility in plan design

- Need improved reporting and claims visibility

- Experience frustration with administrative service

- Receive recommendations from a trusted broker

- Want greater control over vendor selection

- Need support managing complex employee benefits

School districts, municipalities, healthcare organizations, employer groups, and growing businesses frequently evaluate TPAs as part of long-term benefits planning.

A TPA can become a valuable operational partner when organizations need greater flexibility, transparency, and administrative support.

Choosing the Right Third-Party Administrator

Not every TPA offers the same capabilities. Employers and brokers should evaluate potential partners based on service quality, experience, technology, and long-term compatibility—not simply price.

Third-Party Administrator Evaluation Checklist

- Experience administering employer health plans

- Expertise in claims administration and employee benefits administration

- Experience as a workers’ compensation administrator

- Strong customer service and member support

- Flexible plan administration services

- Reporting and analytics capabilities

- Technology integration with pharmacy benefit manager (PBM) partners, PPO networks, and stop-loss insurance providers

- Proven broker partnerships

- Compliance knowledge related to ERISA and HIPAA

- Ability to coordinate medical claims processing, utilization management, and case management

- Long-term relationship focus

For many employers and brokers, responsiveness and communication become just as important as technology. An experienced administrator that acts as an extension of the client’s team can help simplify complex administrative responsibilities while supporting evolving organizational goals.

As an independent claims administrator, Gulf South Risk Services emphasizes personalized service, flexible vendor integration, experienced claims professionals, and long-term partnerships built around each client’s needs rather than standardized carrier models.

The best TPA is one that aligns with your organization’s goals, communicates effectively, and offers the flexibility to support your benefits strategy over time.

Final Thoughts

Understanding what does a third-party administrator do is about much more than understanding claims processing. A modern TPA serves as an operational partner that coordinates health plan administration, employee benefits administration, claims administration, vendor relationships, reporting, customer service, and care management across an employer’s benefit program.

For organizations evaluating self-funded strategies or looking to improve administrative efficiency, an experienced independent TPA can provide greater flexibility, transparency, and support without changing the employer’s overall benefits objectives.

Whether you’re an employer exploring administration options or a broker seeking a collaborative partner, understanding the role of a TPA can help you make more informed decisions about the future of your benefits program.

To learn more about Gulf South Risk Services‘ administration solutions, explore our Health Plan Administration, Workers’ Compensation Programs, Claims Administration & Risk Management, Cost Containment & Plan Optimization, Technology & Vendor Integration, Care Management & Member Support, and For Brokers resources—or contact our team to discuss your organization’s needs.

Frequently Asked Questions

What is a third-party administrator?

A third-party administrator is an organization that manages the day-to-day administration of employer health plans and workers’ compensation programs. TPAs typically oversee claims administration, eligibility, customer service, reporting, vendor coordination, and benefits administration without acting as the insurance company.

Who hires a TPA?

Employers, municipalities, school districts, healthcare organizations, self-funded employer groups, and employee benefits brokers commonly work with TPAs to administer health plans and workers’ compensation programs.

What is the difference between a TPA and an insurance company?

An insurance company generally assumes financial risk under a fully insured plan. A TPA administers the plan, manages operations, and supports employers, but typically does not insure the risk or issue insurance policies.

Do TPAs pay claims?

In most self-funded health plan arrangements, the employer funds eligible claims while the TPA administers the claims process. Under fully insured plans, the insurance carrier generally pays covered claims.

Can a small business use a TPA?

Yes. Organizations of many sizes may work with a TPA depending on their benefit strategy, administrative needs, and plan structure. There is no universal size requirement.

Why do brokers recommend TPAs?

Many brokers value independent TPAs because they offer administrative expertise, flexible vendor coordination, responsive customer service, and support for customized benefit programs while allowing brokers to maintain strong client relationships.

What industries commonly use TPAs?

TPAs support organizations across numerous industries, including healthcare, education, manufacturing, municipalities, public entities, professional services, and private employers that sponsor employee health plans or workers’ compensation programs.