Healthcare costs continue to rise, leading many employers to reevaluate how they structure and manage employee benefits. As organizations look for more flexibility, transparency, and control over healthcare spending, interest in the Self Funded Health Plan model has grown significantly. Employers across multiple industries are exploring alternatives to traditional insurance arrangements in an effort to better align healthcare strategies with organizational goals.

A self-funded approach can offer opportunities for improved visibility into claims activity and healthcare utilization, but it also introduces additional financial and administrative considerations. Understanding how self-funded plans operate is essential before making any decisions.

This article explains how Self Funded Health Insurance works, the role of a Third Party Administrator, the potential advantages and challenges of self-funding, and the factors organizations should evaluate when considering this type of benefit structure.

Have questions about self-funded health plans? Contact Gulf South Risk Services to discuss your organization’s employee benefits goals.

What Is a Self Funded Health Plan?

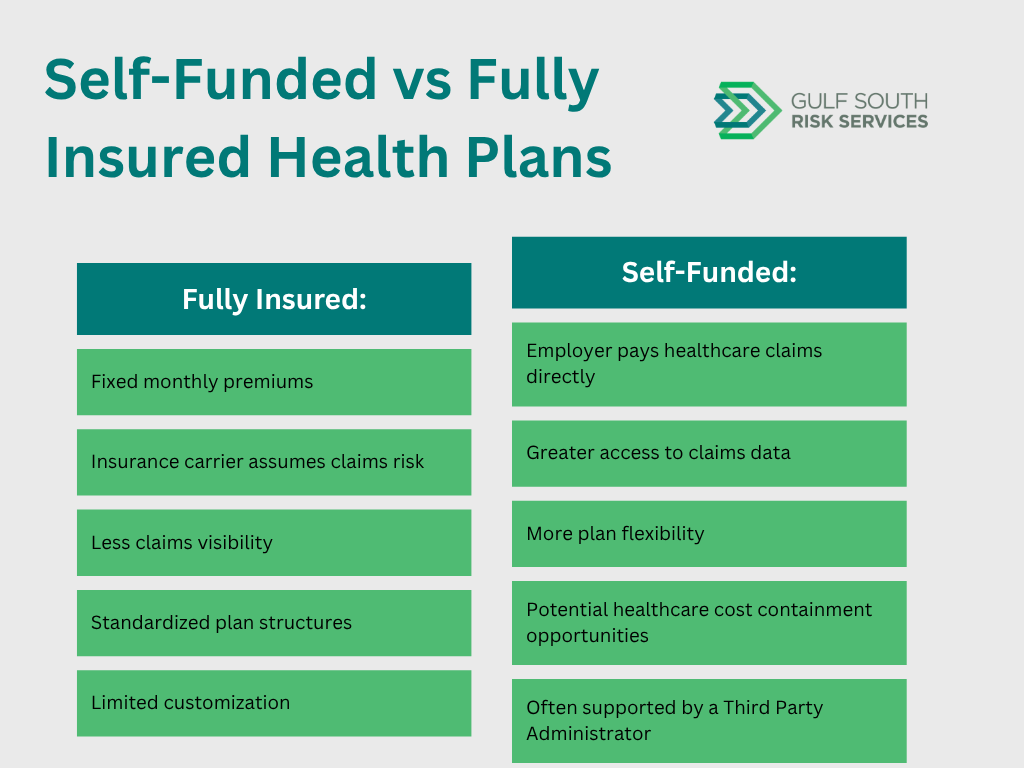

A Self Funded Health Plan is a type of employer-sponsored benefit arrangement in which the employer pays employee healthcare claims directly rather than paying fixed monthly premiums to a traditional insurance carrier.

With traditional fully insured coverage, employers pay premiums to an insurance company that assumes responsibility for healthcare claims. In contrast, a Self Insurance Health Plan places the financial responsibility for claims costs on the employer.

Under this structure, employers typically establish a healthcare fund used to pay medical claims as they occur. While the employer assumes more responsibility, self-funding may also provide greater access to claims data, plan flexibility, and cost visibility.

Many organizations also purchase stop-loss insurance to help protect against large or unexpected claims.

How Self Funded Health Plans Work

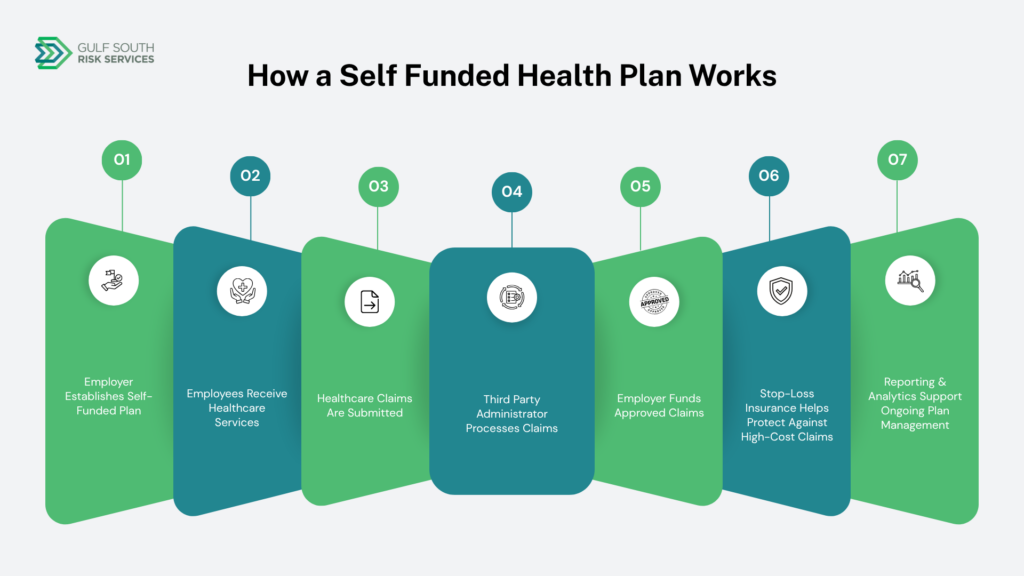

A Self Funded Health Insurance arrangement generally involves several moving parts working together to support employees and manage claims effectively.

The employer funds healthcare claims directly while partnering with vendors and administrators to manage daily operations. This process often includes:

- Claims administration

- Provider network access

- Employee benefits administration

- Pharmacy benefit management

- Compliance support

- Reporting and analytics

- Healthcare claims oversight

Because administering healthcare plans can be complex, many organizations work with a Third Party Administrator (TPA) to help coordinate operations and ensure efficient plan management.

Self-funded plans can also be customized more extensively than many traditional insurance plans, allowing employers to align benefits with workforce needs and organizational priorities.

What Role Does a Third Party Administrator Play?

A Third Party Administrator provides operational and administrative support for self-funded benefit plans. Many employers rely on TPA Services to manage the day-to-day responsibilities associated with healthcare plans.

Common Self Funded Plan Administration services include:

- Claims processing and adjudication

- Member support and customer service

- Eligibility and enrollment management

- Benefits administration

- Regulatory compliance assistance

- Reporting and claims analytics

- Healthcare cost containment support

- Vendor coordination

A TPA can also help employers navigate changing regulations, monitor claims trends, and improve overall plan performance.

Organizations often choose an experienced administrator because effective Health Plan Administration requires specialized expertise, technology integration, and ongoing oversight.

Internal resources:

- What Does a Third Party Administrator Do?

- How TPAs Support Self Funded Health Plans

- Employee Benefits Administration Services

- Claims Administration Services

- Potential Advantages of Self Funding

Many employers explore Self Funded Employee Benefits because of the flexibility and transparency this model may provide.

Greater Cost Transparency

Self-funded plans often provide employers with direct access to healthcare claims data and utilization trends. This visibility may help organizations better understand where healthcare dollars are being spent.

More Plan Flexibility

Unlike many traditional insurance arrangements, self-funded plans can often be tailored to meet specific workforce needs and organizational goals.

Access to Claims Data

Detailed reporting can help organizations identify cost drivers, utilization patterns, and opportunities for program improvements.

Potential Healthcare Cost Containment Opportunities

Self-funded employers may have more flexibility to implement Healthcare Cost Containment strategies such as:

- Utilization review

- Case management

- Provider network optimization

- Pharmacy management programs

- Claims auditing

While potential savings are often discussed, results vary by organization and depend on factors such as claims experience, workforce demographics, and plan design.

Considerations Before Moving to a Self Funded Plan

Although self-funding may offer advantages, it is not the right solution for every organization.

Claims Volatility

Employers assume responsibility for healthcare claims costs, which can fluctuate from year to year.

Cash Flow Requirements

Organizations must be prepared to fund claims as they occur, including potentially large or unexpected expenses.

Administrative Responsibilities

Managing Employer Sponsored Health Plans requires coordination among vendors, administrators, and internal stakeholders.

Risk Management

Employers should evaluate financial reserves, stop-loss coverage, and long-term benefit strategies before transitioning to a self-funded arrangement.

Every organization’s situation is different, and a thorough evaluation is important before making a decision.

Understanding Stop-Loss Insurance

Stop-loss insurance is commonly used alongside self-funded plans to help manage financial risk.

There are generally two primary forms of stop-loss coverage:

Individual Stop-Loss

Protects against high-cost claims incurred by a single participant.

Aggregate Stop-Loss

Protects against total claims costs exceeding a predetermined threshold for the entire plan.

Many employers ask whether stop-loss insurance eliminates risk entirely. While it can reduce exposure to catastrophic claims, employers still retain responsibility for certain plan costs and ongoing administration.

Which Organizations Commonly Consider Self Funding?

A variety of organizations evaluate self-funded structures, including:

- Mid-sized employers

- Large employers

- Municipalities

- School districts

- Healthcare organizations

- Public entities

- Private organizations

There is no universal size requirement for self-funding. Organizations often evaluate factors such as workforce demographics, claims history, financial objectives, and benefit goals when considering this approach.

Questions Employers Should Ask Before Making a Decision

Organizations evaluating a self-funded approach should consider several important questions:

- Do we understand our claims experience?

- Are healthcare costs increasing?

- What are our employee benefit goals?

- How much flexibility do we need?

- What level of risk are we comfortable assuming?

- Do we have the right administrative support?

- How important is access to claims data and reporting?

A thorough evaluation can help employers understand whether self-funding aligns with their goals and risk profile.

Common Misconceptions About Self Funded Health Plans

Self-Funding Is Only for Large Corporations

While large employers frequently self-fund, many mid-sized organizations also explore self-funded options.

Self-Funding Eliminates Risk

Self-funding does not eliminate risk. Employers assume claims responsibility, although stop-loss insurance may help reduce exposure.

Self-Funded Plans Require Employers to Manage Everything Internally

Many organizations partner with a Third Party Administrator for claims administration, reporting, and operational support.

Self-Funded Plans Are the Same as Traditional Insurance

Self-funded arrangements operate differently because employers fund claims directly rather than paying fixed premiums to transfer risk entirely to an insurance carrier.

How to Evaluate Whether Self Funding Is Right for Your Organization

Employers considering self-funding should take a structured approach to evaluation.

Important considerations may include:

- Historical claims experience

- Workforce demographics

- Financial objectives

- Long-term benefit strategy

- Administrative resources

- Vendor partnerships

- Risk tolerance

- Healthcare utilization trends

Organizations should also evaluate the role that experienced TPA Services and Employee Benefits Administration support can play in maintaining plan performance and operational efficiency.

A balanced review of both opportunities and responsibilities can help employers make informed decisions regarding self-funded healthcare strategies.

Frequently Asked Questions

What is a self-funded health plan?

A self-funded health plan allows an employer to pay employee healthcare claims directly instead of purchasing traditional fully insured coverage.

How is self-funding different from traditional insurance?

With traditional insurance, employers pay fixed premiums to a carrier. With self-funding, employers assume responsibility for healthcare claims costs.

What does a Third Party Administrator do?

A Third Party Administrator helps manage claims administration, benefits administration, reporting, compliance support, and other operational responsibilities.

What is stop-loss insurance?

Stop-loss insurance helps protect self-funded employers from catastrophic or excessive healthcare claims costs.

Are self-funded plans only for large employers?

No. Organizations of varying sizes may consider self-funded structures depending on their goals, financial position, and workforce characteristics.

Conclusion

A Self Funded Health Plan can provide organizations with greater flexibility, transparency, and visibility into healthcare spending. However, self-funding also involves additional financial responsibility, administrative coordination, and risk management considerations.

Organizations evaluating Employer Sponsored Health Plans should carefully assess claims history, workforce needs, long-term objectives, and operational capabilities before making a decision. Working with experienced professionals can help employers better understand both the opportunities and responsibilities associated with self-funded healthcare arrangements.

Contact Gulf South Risk Services to learn more about self-funded health plans, claims administration, and employee benefits solutions for your organization.